Starting April 18, 2026, the Visa Subscription Management Rule will require European banks to allow debit card users to find, stop, and reactivate future payments directly in their online banking platform or mobile app. Banks cannot require customers to make phone calls to cancel payments, and must provide a digital self-service option. This allows customers to instantly cancel future charges without involving the merchant.

This update is critical for agents managing recurring revenue portfolios across Europe.

Visa Rule 0031078 only applies to consumer debit cards in Belgium, Croatia, Czech Republic, France, Hungary, Italy, Luxembourg, Poland, Republic of Ireland, Romania, Slovakia, Slovenia, and United Kingdom. This rule does not apply to credit or business cards.

This impacts any automatic payment, including:

When a customer blocks payments in their bank app, the merchant will receive new hard decline codes:

Banks must inform cardholders that blocking a payment in their app does not cancel their contract with the merchant. However, the payment will still result in a hard decline, leaving the merchant responsible for collecting any outstanding balance outside the automated billing process.

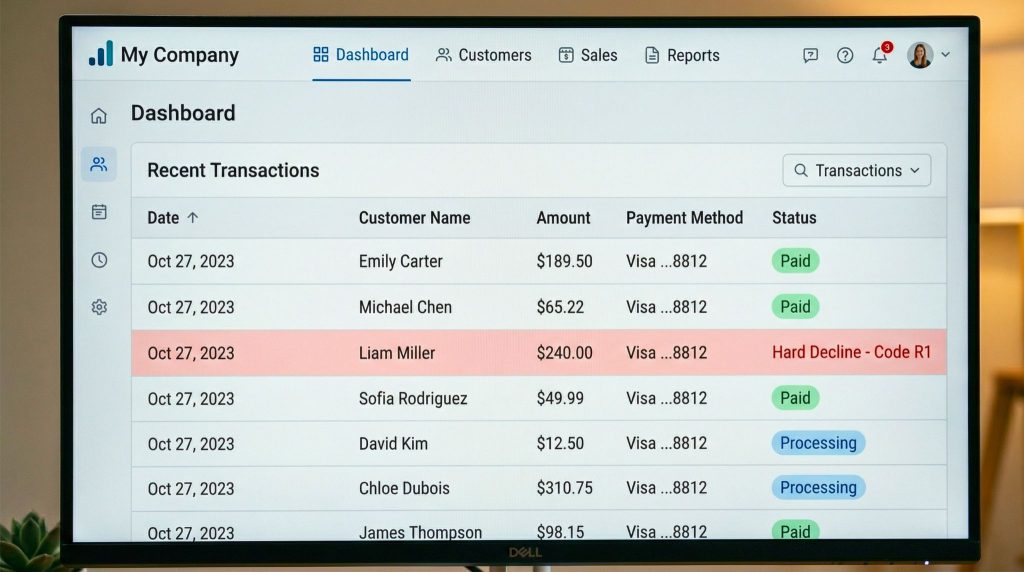

Under Visa Rule 0031078, customers can block a payment before it happens. Since the transaction never goes through, a chargeback cannot be filed. What would have been a dispute becomes a declined authorization.

The risk comes from how you handle that decline. Visa penalizes poor authorization quality and excessive retry attempts. Many merchants use automated dunning tools that repeatedly retry declined cards. If a customer revokes authorization (triggering an R1 or R3 decline) and your system continues retrying, Visa will flag this behavior.

Repeated attempts on revoked cards can lower your VAMP authorization score and may lead to non-compliance fines.

Read about the latest VAMP update.

Agents, ISOs, and acquirers play a critical role in helping merchants adapt to Visa Rule 0031078 and avoid unnecessary risk. The following options are not impacted by this rule and can improve long-term payment success rates:

Visa’s announcements of this rule have been limited to select European markets. However, similar consumer-first controls could expand to the US. As regulatory and network trends continue to prioritize transparency and self-service payment management. Agents should monitor developments closely and begin preparing merchants for the potential of similar changes coming to the US in the future.

As Visa shifts control to consumers, an increase of blocked payments and hard declines will impact merchant performance and authorization quality. Agents who proactively update authorization decline logic, guide merchants on compliance, and implement alternative payment and recovery strategies, will protect approvals and recurring revenue streams. Those who adapt early will strengthen their portfolios and gain a competitive edge.

Overall, this rule may reduce chargebacks, but it can also lower merchant ROI by hurting customer retention. It shifts more control to the customer, allowing them to cancel subscriptions instantly. However, this creates a new risk, as customers may not recognize billing descriptors and accidentally cancel active subscriptions, leading to unintended revenue loss.

The information provided here is for informational purposes only and focuses solely on payment processing in the cannabis industry. We do not endorse explicit or illegal content and encourage compliance with applicable laws and regulations. Readers should seek professional advice and use legitimate payment solutions while operating in this sector. We disclaim liability for any consequences resulting from the use of this information.