“[F]irst-party fraud—consumers defrauding organizations—remains the leading source of fraud globally for the second consecutive year. First-party fraud accounted for 38.3% of all reported fraud in 2025… 30% of fraud activity reported in 2025 came from first-party fraud in the USA. A 22% increase from 2024 (LexisNexis).” First party fraud spans all generations, but the majority are conducted by people in their 40’s or younger. This demonstrates that generational economics plays a role in the severity of first party fraud.

First-party fraud occurs when a customer directly purchases a product or service. After the purchase, the same customer disputes the transaction with their bank, or utilizes one of many deceitful tactics, to avoid payment on goods they wish to use. Essentially returning their funds to their card or bank account, while retaining any goods/services acquired from the purchase.

In an attempt to protect customers, some issuing banks are making it easy for people to file chargebacks. In some cases, customers can easily defraud merchants by opening their banking app and filing chargebacks. This creates a low effort, easy fraud attack vector that many can easily take advantage of. Even when merchants successfully overturn chargebacks, they still absorb any chargeback fees. For agents, merchants unable to manage their chargeback ratios are at risk of account termination, a threat to long-term residuals.

A customer uses a business’ refund policy to take advantage of the merchant, and in some cases defrauding the merchant to keep their ill-gotten gains. Below are some common examples of return fraud:

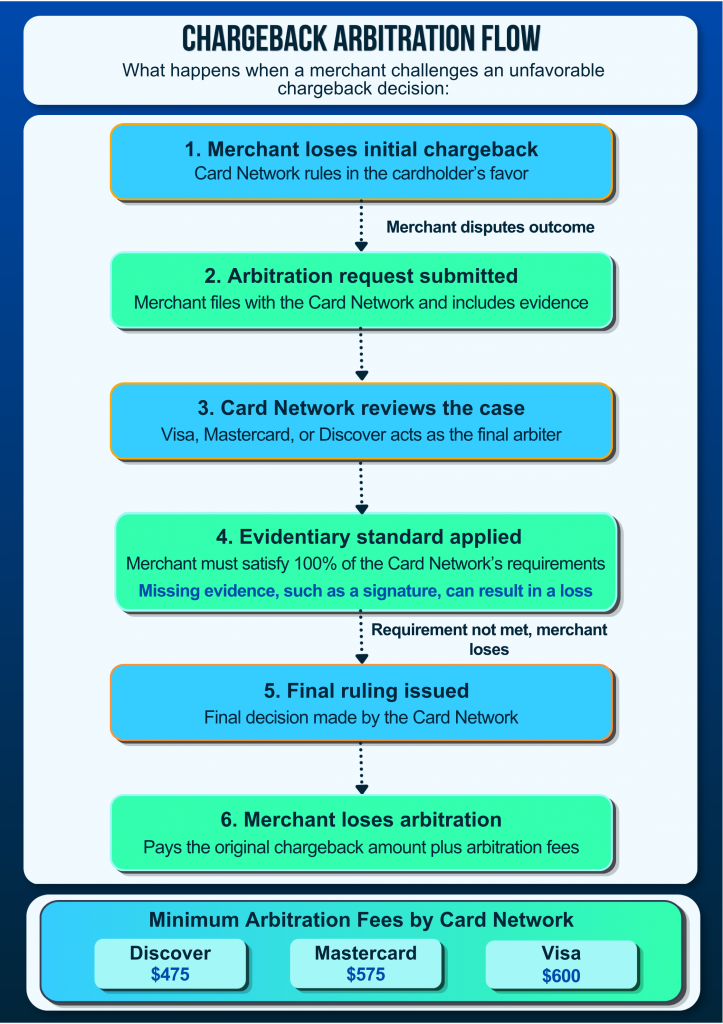

A customer orders a product online, receives it, but falsely claims they did not receive the package and files a chargeback. Without signature delivery confirmation from the cardholder, the merchant cannot win a non-delivery dispute, despite possessing supporting email evidence. If the dispute proceeds to arbitration, the merchant loses both the chargeback amount and a minimum arbitration fee (Discover: $475, Mastercard: $575, Visa: $600). Signature delivery confirmation by the cardholder is a standard requirement to successfully dispute a non-delivery chargeback. For example, if a merchant delivers a product without signature delivery a customer can file a chargeback claiming non-delivery. Despite submitting evidence demonstrating delivery during the rebuttal process, merchants still lose at the chargeback arbitration phase. This is because cardholder signature confirmation is required to successfully dispute a non-delivery claim.

A client leverages false, or partially false, info to receive rewards. For instance, a merchant offers a free 30-day trial to new customers. A customer then opens new accounts every month to take advantage of the offer.

A customer falsely claims they do not recognize a transaction on their bank statement, due to their inability to recall the purchase correctly. For example, a customer purchases a supplement from an online store. After receiving the supplement, the customer claims the charge on their statement is unrecognized and is therefore unauthorized.

A customer’s family member makes a purchase using the account holder’s payment information. Afterwards, the true account holder disputes the charge, claiming the transaction was unauthorized. For example, a customer uses a parent’s credit card to buy something. When the parent discovers the transaction, they claim to have never made the purchase.

A customer intentionally misrepresents their identity, or provides false information, to get a product or service. For instance, a customer who’s been flagged for prior incidents of return fraud creates a new account using false information, enabling them to continue making their fraudulent returns.

Involves intermediaries receiving or transporting stolen and fraudulently obtained funds. For example, a mule may issue a fraudulent check. Then withdraw funds from the respective bank account.

A customer uses an authentic identity to build trust, then defaults across multiple accounts. As an example, a customer builds up 2 credit cards, eventually unlocking high credit limits. After keeping the balance low, the customer suddenly spends up to their limits and never pays the balance.

People on social media are now coordinating shared fraud tactics, then executing them simultaneously. For instance, a viral video circulates, showing viewers how to exploit a software company’s free trial offering. Across various online gatherings, users share their workarounds and how to fake account details. Costing the company thousands in lost revenue.

Elite Pay will work with you and merchants to determine effective fraud counter measures and discuss options with you. These protections are more or less viable depending on the merchant’s sales volume. Here is how to protect your merchant/business:

There are several methods to detect first party fraud:

First-party fraud is one of the fastest growing threats merchants face. Without the right policies and tools in place, your merchants are absorbing losses on disputes they can’t win. We help connect merchants with the necessary protections that fit their sales volume and risk profile.

The information provided here is for informational purposes only and focuses solely on payment processing. We do not endorse explicit or illegal content and encourage compliance with applicable laws and regulations. Readers should seek professional advice and use legitimate payment solutions while operating in this sector. We disclaim liability for any consequences resulting from the use of this information.